The collections playbook in most Indian banks and NBFCs hasn't fundamentally changed in fifteen years. High-volume calling. Scripted follow-ups. Agents chasing accounts across a predictive dialler. Repeat until paid or written off.

The problem: the environment around that playbook has changed completely. And the old approach is now actively creating problems it was never designed to handle.

What's Changed Since 2010 That Collections Teams Haven't Caught Up To

1. Regulatory exposure is real now

RBI guidelines on collections conduct are detailed, enforceable, and getting stricter. A single agent calling outside permitted hours or using language outside guidelines is no longer a training issue. It's a compliance event.

2. Borrowers know their rights

Today's borrower knows they can complain to the RBI ombudsman. They know what harassment means legally. And they know how to document it. The era of aggressive collections flying under the radar is over.

3. The phone isn't the only channel

A borrower who doesn't answer a call may respond to a WhatsApp message immediately. Collections strategies still built entirely around voice calling are leaving recovery on the table.

4. Data exists to be smarter

Banks today have transaction behavior, income signals, and interaction history that could predict which borrowers will self-cure, which need a payment plan conversation, and which need immediate escalation. Most collections operations use none of it.

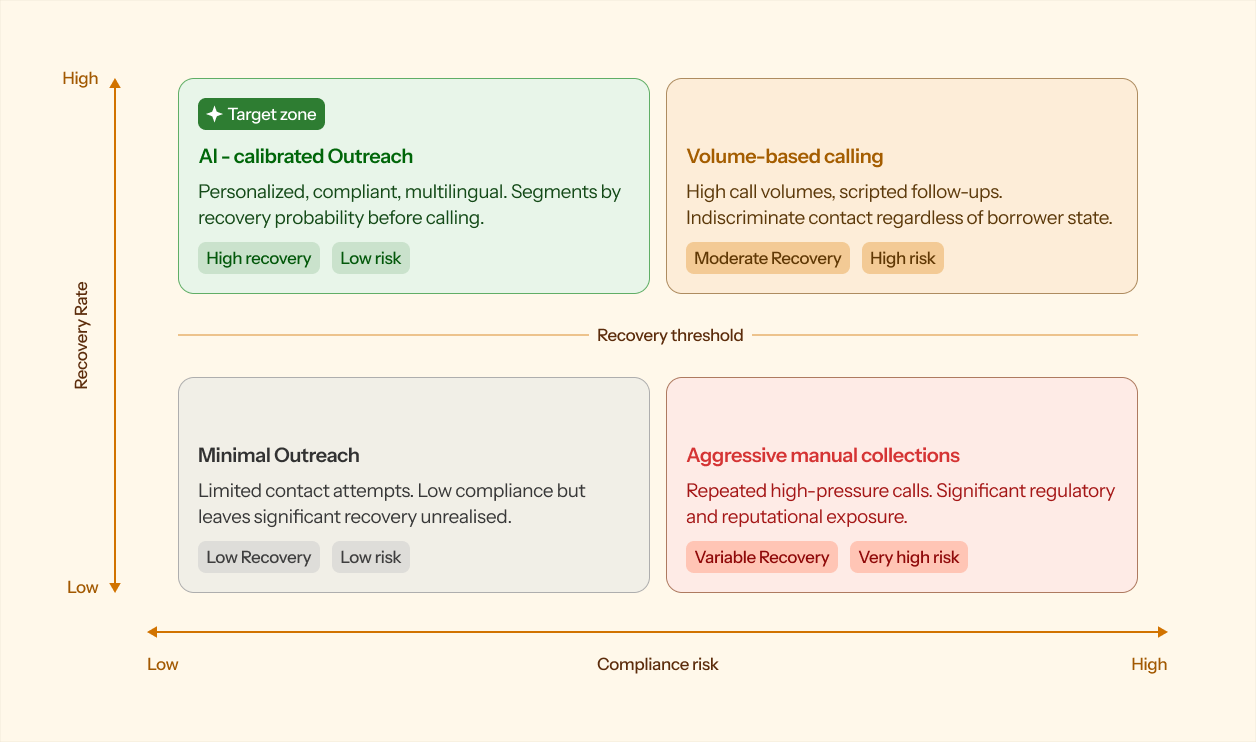

The Core Problem with Volume-Based Collections

The traditional model assumes: contact enough borrowers enough times, and a sufficient percentage will pay. The strategy is persistence.

This creates two compounding problems.

It's indiscriminate. A borrower who missed a payment due to a temporary cash flow issue, and will self-cure within days, receives the same contact intensity as one who is genuinely unable to pay. That contact damages the first borrower's relationship without adding recovery value.

It's regulatorily fragile. At high volume, the probability of a compliance event, wrong timing, wrong language, wrong contact, is not small. It's predictable.

What AI Voice Agents Do Differently in Collections

AI voice agents don't replace human judgment on complex cases. They do everything else, and they do it in a way that is structurally more compliant and more precise than human calling at scale.

The Bottom Line

The collections playbook from 2010 is creating regulatory risk and relationship damage in 2026. Not because the goal changed, recovering overdue payments remains essential, but because the environment has.

AI voice agents that calibrate contact strategy to individual borrower circumstances, maintain compliance at scale, and communicate in the right language are not an upgrade to collections. They are the new operating baseline for any BFSI institution that wants to recover debt without building regulatory exposure in the process.